[MOST PEOPLE THINK THEY’RE COVERED. THEY’RE NOT.]

Discover How Our LifeFlexi™ Pro Strategy Can Give You 6 To 7 Figures That Will Change Your Life

Premiums rise. Health declines. Eligibility disappears.

Clarity today costs less than regret tomorrow.

This Isn’t About Insurance.

It’s About What Happens If You’re Wrong.

Because most people don’t realise they’re exposed…

until something forces them to find out.

Inside This Session, You’ll Discover:

How one small monthly decision (less than a Kopi-O a day) could mean the difference between a six-figure payout — or six-figure regret

The structural mistake most working professionals make before 35 that leaves them either overpaying or dangerously under-covered

Whether the upcoming hospital plan changes in 2026 will increase your out-of-pocket risk — and how to avoid draining your savings when it matters most.

If your current plan actually ringfences your wealth… or slowly cannibalises it.

[MOST PEOPLE THINK THEY’RE COVERED. THEY’RE NOT.]

Discover How Our LifeFlexi™ Pro Strategy Can Give You 6 To 7 Figures That Will Change Your Life

Premiums rise. Health declines. Eligibility disappears.

Clarity today costs less than regret tomorrow.

This Isn’t About Insurance.

It’s About What Happens If You’re Wrong.

Because most people don’t realise they’re exposed…

until something forces them to find out.

Inside This Session, You’ll Discover:

How one small monthly decision (less than a Kopi-O a day) could mean the difference between a six-figure payout — or six-figure regret

The structural mistake most working professionals make before 35 that leaves them either overpaying or dangerously under-covered

Whether the upcoming hospital plan changes in 2026 will increase your out-of-pocket risk — and how to avoid draining your savings when it matters most.

If your current plan actually ringfences your wealth… or slowly cannibalises it.

If you're here today... You have to read this.

(Scroll down to try out our 'Daily Coffee Calculator')

Most people in Singapore think they’re protected.

They say things like:

•“I have hospital plan.”

“Got CI already.”

“My agent settled for me.”

But ask them:

"How much exactly will you receive?"

"How long can you survive without income?"

"Are you overpaying?"

"Are you under-insured?"

"Are you structurally exposed?"

Silence.

Because what most people own… is a collection of policies.

Not a financial defence system.

I met a prospect once. He Wanted to Buy a Critical Illness Plan.

He worked his job, had a sister he was close to, and had goals to work towards. He understood the logic of protection after hearing real-life scenarios from his friends. He knew that if something serious happened, insurance would be the difference between inconvenience and financial devastation.

He was just like you. He clicked on the advertisement. He reached out.

We spoke. We discussed coverage amounts. We looked at structures. He agreed it made sense.

He just needed a little more time to "sort things out". Work was busy.

Deadlines were piling up. Appointments with him kept shifting.

“Let’s do it soon,” he said.

That was the last proper conversation we had.

More than half a year later, when I followed up again, I wasn’t told he was still busy.

His sister was the one that picked up the phone and told me he was in the hospital.

Stage 3 Chronic Myeloid Leukemia.

And suddenly, we weren’t talking about structuring protection anymore. We were talking about what could have been done — and what could no longer be changed. Because once a diagnosis happens, insurance stops being planning.

It becomes regret.

Most people assume they have time. They assume illness is something that happens to “other people.”

They assume protection is something that can be handled next quarter.

They assume their current policies are “good enough.”

But statistics in Singapore don’t support that comfort.

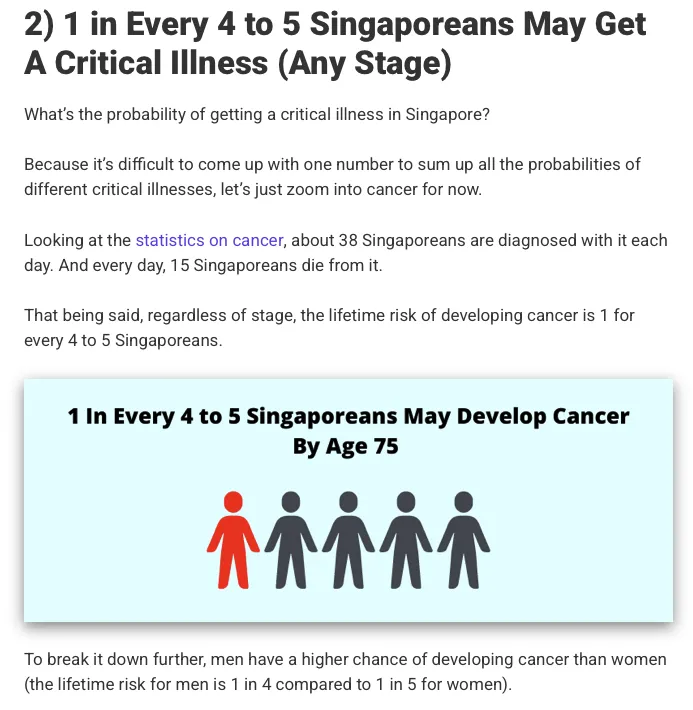

1 in 3 Singaporeans will be diagnosed with a critical illness before age 60.

That is not rare. That is probability.

And yet, studies consistently show that the majority of working adults are either underinsured for critical illness or do not have coverage that adequately replaces income.

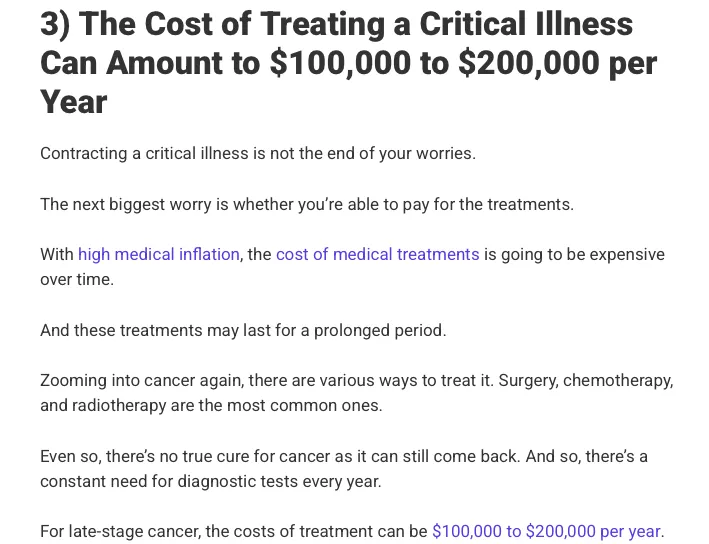

Most people plan for hospital bills.

Very few plan for income disruption, which is often the real financial killer.

Because medical bills can be partially insured.

But what about:

Months or years of reduced earning capacity?

Career progression interrupted?

Investments liquidated prematurely?

Mortgage payments continuing?

Dependents still relying on you?

When income stops, life does not.

The Real Risk Isn’t Illness. It’s Financial Unpreparedness.

When someone faces a critical illness, the financial damage usually comes from three places:

1. Loss of income.

2. Underestimated out-of-pocket costs.

3. Poorly structured protection.

And here is the part that is uncomfortable:

Most people who think they are “covered” discover gaps only when we run their numbers.

They assume the sum assured is sufficient. They assume hospital plans solve everything.

They assume having “a policy” means they are protected.

But coverage without structure is like owning bricks without architecture.

It exists — but it may not hold.

Age increases premiums. Health conditions reduce eligibility. Diagnoses eliminate options.

You can earn more money over time. You cannot rewind your medical history.

And once underwriting closes the door, there is no appeal based on good intentions.

The Rules Are Changing

Hospital rider structures are shifting in 2026. Deductible waivers are being removed. Co-payment caps are increasing.

Policies purchased today may be transitioned to new structures later.

This means even people who believe they are protected may face higher out-of-pocket exposure in the future.

Doing nothing is no longer neutral.

It is a decision to accept unknown exposure.

Let Me Be Clear About Something

This is not about fear.

It is about leverage.

Right now, if you are healthy, you have negotiating power.

You have options.

You can choose structure deliberately.

After diagnosis, you lose that leverage entirely.

That is not dramatic exaggeration.

That is underwriting reality.

What Our LifeFlexi™ Pro Strategy Actually Does

This is not a “buy now” session.

It is a structured Financial Risk Diagnostic that answers one uncomfortable but necessary question:

“If something serious happens tomorrow, does my plan hold — or does my wealth unravel?”

We go through:

Your current financial standing.

Your real income vulnerability.

Your cash flow reality.

Your coverage efficiency.

Most people walk away surprised.

Not because they have nothing.

But because they realise they were never shown the full picture.

Ask Yourself Honestly

If something happened within the next 12 months:

Would your savings survive? Would your family’s lifestyle remain intact? Would you still feel dignified — or dependent?

Would you be confident… or scrambling?

If you cannot answer those clearly, then you do not have clarity.

And clarity is not something you want to delay.

The Hard Truth

The most expensive insurance policy is not the one with the highest premium.

It is the one you buy too late.

Because at that point, you pay more for less — or you pay everything out-of-pocket.

You worked too hard to build what you have.

You sacrificed too much time to earn it.

Protecting it is not optional.

It is responsible.

Right now, you have leverage.

You have health.

You have options.

The only question is whether you will act while those three still exist.

👉 Book Your Coverage Risk Check Now

Don't wait,

Ben

If you're here today... You have to read this.

(Scroll down to try out our 'Daily Coffee Calculator')

Most people in Singapore think they’re protected.

They say things like:

•“I have hospital plan.”

“Got CI already.”

“My agent settled for me.”

But ask them:

"How much exactly will you receive?"

"How long can you survive without income?"

"Are you overpaying?"

"Are you under-insured?"

"Are you structurally exposed?"

Silence.

Because what most people own… is a collection of policies.

Not a financial defence system.

I met a prospect once. He Wanted to Buy a Critical Illness Plan.

He worked his job, had a sister he was close to, and had goals to work towards. He understood the logic of protection after hearing real-life scenarios from his friends. He knew that if something serious happened, insurance would be the difference between inconvenience and financial devastation.

He was just like you. He clicked on the advertisement. He reached out.

We spoke. We discussed coverage amounts. We looked at structures. He agreed it made sense.

He just needed a little more time to "sort things out". Work was busy.

Deadlines were piling up. Appointments with him kept shifting.

“Let’s do it soon,” he said.

That was the last proper conversation we had.

More than half a year later, when I followed up again, I wasn’t told he was still busy.

His sister was the one that picked up the phone and told me he was in the hospital.

Stage 3 Chronic Myeloid Leukemia.

And suddenly, we weren’t talking about structuring protection anymore. We were talking about what could have been done — and what could no longer be changed. Because once a diagnosis happens, insurance stops being planning.

It becomes regret.

Most people assume they have time. They assume illness is something that happens to “other people.”

They assume protection is something that can be handled next quarter.

They assume their current policies are “good enough.”

But statistics in Singapore don’t support that comfort.

1 in 3 Singaporeans will be diagnosed with a critical illness before age 60.

That is not rare. That is probability.

And yet, studies consistently show that the majority of working adults are either underinsured for critical illness or do not have coverage that adequately replaces income.

Most people plan for hospital bills.

Very few plan for income disruption, which is often the real financial killer.

Because medical bills can be partially insured.

But what about:

Months or years of reduced earning capacity?

Career progression interrupted?

Investments liquidated prematurely?

Mortgage payments continuing?

Dependents still relying on you?

When income stops, life does not.

The Real Risk Isn’t Illness. It’s Financial Unpreparedness.

When someone faces a critical illness, the financial damage usually comes from three places:

1. Loss of income.

2. Underestimated out-of-pocket costs.

3. Poorly structured protection.

And here is the part that is uncomfortable:

Most people who think they are “covered” discover gaps only when we run their numbers.

They assume the sum assured is sufficient. They assume hospital plans solve everything.

They assume having “a policy” means they are protected.

But coverage without structure is like owning bricks without architecture.

It exists — but it may not hold.

Age increases premiums. Health conditions reduce eligibility. Diagnoses eliminate options.

You can earn more money over time. You cannot rewind your medical history.

And once underwriting closes the door, there is no appeal based on good intentions.

The Rules Are Changing

Hospital rider structures are shifting in 2026. Deductible waivers are being removed. Co-payment caps are increasing.

Policies purchased today may be transitioned to new structures later.

This means even people who believe they are protected may face higher out-of-pocket exposure in the future.

Doing nothing is no longer neutral.

It is a decision to accept unknown exposure.

Let Me Be Clear About Something

This is not about fear.

It is about leverage.

Right now, if you are healthy, you have negotiating power.

You have options.

You can choose structure deliberately.

After diagnosis, you lose that leverage entirely.

That is not dramatic exaggeration.

That is underwriting reality.

What Our LifeFlexi™ Pro Strategy Actually Does

This is not a “buy now” session.

It is a structured Financial Risk Diagnostic that answers one uncomfortable but necessary question:

“If something serious happens tomorrow, does my plan hold — or does my wealth unravel?”

We go through:

Your current financial standing.

Your real income vulnerability.

Your cash flow reality.

Your coverage efficiency.

Most people walk away surprised.

Not because they have nothing.

But because they realise they were never shown the full picture.

Ask Yourself Honestly

If something happened within the next 12 months:

Would your savings survive? Would your family’s lifestyle remain intact? Would you still feel dignified — or dependent?

Would you be confident… or scrambling?

If you cannot answer those clearly, then you do not have clarity.

And clarity is not something you want to delay.

The Hard Truth

The most expensive insurance policy is not the one with the highest premium.

It is the one you buy too late.

Because at that point, you pay more for less — or you pay everything out-of-pocket.

You worked too hard to build what you have.

You sacrificed too much time to earn it.

Protecting it is not optional.

It is responsible.

Right now, you have leverage.

You have health.

You have options.

The only question is whether you will act while those three still exist.

👉 Book Your Coverage Risk Check Now

Don't wait,

Ben

The Daily Coffee Calculator

Small daily expenses, massive long-term impact

ARTICLES

Here's why you're running out of time.

TESTIMONIALS

What others are saying

"Highly recommend this"

"Honestly, I thought it was just another insurance talk. But after chatting with The Side Bar, I realised there were so many things I didn’t know about my own coverage. He explained everything so clearly, no pressure, no hard sell. I walked away feeling a lot more confident about where I stand."

– Sharon L., 35

"I didn't know till I was shown"

"I’ve been with the same policy my friend sold me years ago and thought I was well covered. The Side Bar showed me exactly what was missing — and it was a huge gap I didn’t even know about. I’m so glad I found out now, rather than when it’s too late. I wish I had done this review earlier."

– Daniel T., 28

"Unbiased planning"

"I always assumed all insurance was the same, but The Side Bar really opened my eyes to what’s actually available today. There are better products now that cost less and cover more than what I was paying for. It’s crazy to think how much I could’ve saved (and been better protected) if I had switched earlier."

– Mei Ying, 44